Key Takeaways:

- A UCC filing is a public notice that protects a lender’s or factoring company’s legal claim on a borrower’s assets or receivables.

- The UCC-1 financing statement is the official document that records this claim, keeping transactions transparent and preventing overlapping liens.

- In freight factoring, UCC filings secure ownership of invoices, prevent double financing, and establish the factor’s priority in case of default.

- Routiqo stands out in 2026 as the best freight factoring company, offering fast funding, transparent rates, and trusted support for owner-operators.

What Does UCC Filing Mean?

A UCC filing is a public notice that a lender has a legal claim on a borrower’s assets. It is filed with the Secretary of State to make other creditors aware that specific property or business assets are being used as collateral for a loan.

This filing does not transfer ownership of the assets but records the lender’s right to claim them if the borrower defaults. It ensures transparency in financial transactions and helps prevent multiple lenders from securing interests in the same collateral.

In essence, the UCC filing meaning revolves around protection and clarity in lending. It safeguards the lender’s interest while informing others that certain assets are already pledged under an existing agreement.

What Are the Types of UCC Filings?

UCC filings generally fall into two categories, depending on how much of a borrower’s property is being used as collateral. The difference lies in whether the lender’s claim is tied to one asset or covers the business as a whole.

1. Specific Collateral Filing

A specific collateral filing focuses on one clearly defined asset that secures a loan, such as a single truck, a piece of equipment, or a customer account. This type of filing keeps things straightforward—the lender’s claim is limited to that particular item, and the rest of the borrower’s assets remain free.

Example: If a company takes a loan to buy one delivery truck, the lender files a UCC statement that covers only that vehicle.

2. Blanket Lien Filing

A blanket lien filing covers nearly everything the borrower owns, including equipment, inventory, and receivables. It gives the lender a much wider safety net, especially for larger or ongoing loans.

Example: A bank offering a $500,000 credit line might file a blanket lien over “all assets of the debtor.” This type of filing is common for small business and SBA loans because it helps reduce the lender’s overall risk.

How UCC Filings Work?

A UCC filing is a legal step lenders take to protect their interest in a borrower’s assets by making the agreement public. It involves three key parties: the borrower who takes the loan, the lender who provides the funds, and the collateral that secures the debt.

The filing uses a UCC-1 financing statement, which includes the names and details of both parties along with a description of the pledged assets. Once submitted to the Secretary of State, it becomes part of public records and stays valid for five years unless it is renewed or terminated.

What Is a UCC-1?

A UCC-1 is the actual form a lender files to make a UCC filing official. It’s submitted to the Secretary of State and serves as public proof that certain assets are being used to secure a loan or line of credit.

Think of it as the document that gives a UCC filing its legal weight. It lists the borrower, the lender, and the assets involved, making the lender’s claim visible to anyone who checks the public record.

What UCC-1 Financing Statement & Who Should File It?

A UCC-1 Financing Statement is the form a lender files to show that a borrower’s assets are being used to secure a loan. It makes the agreement public, showing which property is pledged and giving the lender a legal claim if the borrower defaults.

This filing acts as a safeguard for the lender and creates transparency for other creditors. It clearly shows who holds a financial interest in the borrower’s assets and helps prevent overlapping claims on the same collateral.

The lender, also called the secured party, is the one responsible for filing the UCC-1 with the Secretary of State. Doing so officially records their interest in the collateral and ensures their rights are protected throughout the loan period.

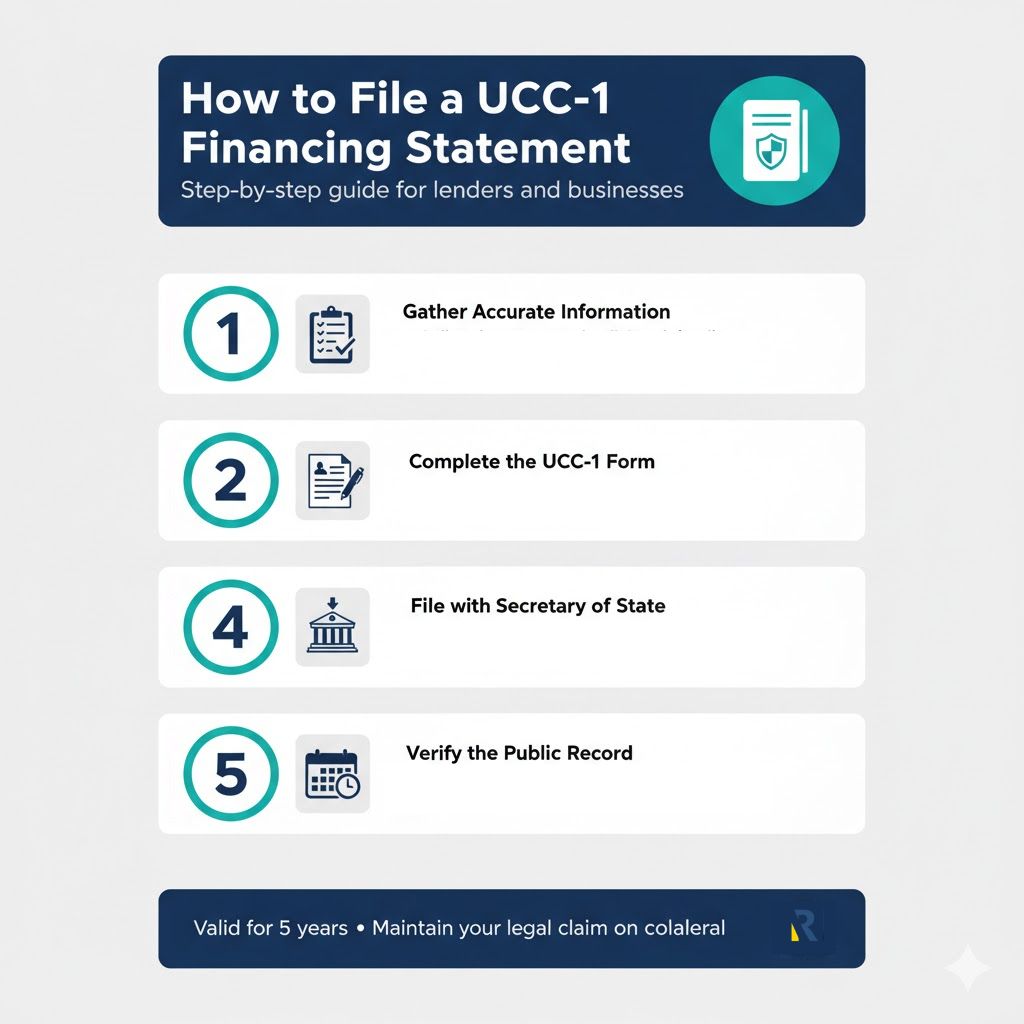

How to File a UCC-1 Financing Statement?

1. Gather Accurate Information

Before filing, the lender must collect complete and correct details about both parties and the collateral. This includes the borrower’s full legal name, business address, and a clear description of the assets being used to secure the loan.

2. Complete the UCC-1 Form

The next step is filling out the official UCC-1 Financing Statement form, which is available through the Secretary of State’s office or its website. The form must include the names and addresses of the borrower and lender, along with an exact description of the collateral to avoid disputes later.

3. File with the Secretary of State

Once the form is ready, the lender files it with the Secretary of State in the state where the borrower’s business is registered. Filing can be done online or by mail, and once submitted, it becomes part of the state’s public record of secured transactions.

4. Verify the Public Record

After the filing is accepted, it’s important to confirm that the record appears correctly in the public database. This verification ensures there are no errors or missing details that could weaken the lender’s legal claim in the future.

5. Monitor and Renew as Needed

A UCC-1 filing remains valid for five years from the filing date. If the loan is still active after that period, the lender must file a UCC-3 continuation statement before the expiration date to maintain their claim on the collateral.

How Much Does It Cost to File a UCC Financing Statement?

The cost to file a UCC financing statement depends on the state where it’s submitted, but it usually ranges between $10 and $50 for standard online filings. Some states charge additional fees for paper submissions or expedited processing, which can bring the total to around $100 in certain cases.

If the filing is done through a third-party service or legal provider, there may be small administrative or service fees added on top of the state’s charge. It’s always best for lenders to check the Secretary of State’s website for the exact filing fee, as rates and methods can vary slightly from state to state.

How Long Does a UCC Filing Last?

A UCC filing typically remains valid for five years from the date it’s filed with the Secretary of State. After that period, the lender must file a UCC-3 continuation statement to keep the filing active and maintain their legal claim on the collateral.

If the lender doesn’t renew before the expiration date, the filing automatically lapses, and the lender’s security interest is no longer protected. Once the loan is fully repaid, the lender files a UCC-3 termination statement to officially remove the lien from public records.

How to Remove or Terminate a UCC Filing?

Confirm the Loan Is Fully Repaid

The first step is to make sure the borrower has met all obligations under the loan or credit agreement. Once the debt is fully settled, the lender no longer has a reason to hold a claim on the borrower’s assets.

Request a UCC-3 Termination Statement

After repayment, the borrower should ask the lender to file a UCC-3 Termination Statement with the Secretary of State. This document officially removes the lender’s claim and signals that the collateral is released.

Verify the Termination in Public Records

Once the UCC-3 is filed, it’s essential to check the public database to confirm the lien no longer appears as active. This verification helps prevent old or inactive filings from affecting future loans or credit opportunities.

Address Any Delays or Errors

If a lender fails to terminate the filing or the record shows incorrect information, the borrower can contact the Secretary of State’s office to request a correction. Keeping the records accurate ensures clean financial standing and protects the business’s borrowing ability.

What Is the Relation Between Factoring Contracts, UCC Filings, and Buyouts?

Factoring contracts, UCC filings, and buyouts are all connected through the way they manage ownership and rights to a company’s receivables or assets. In a factoring agreement, a business sells its unpaid invoices to a factoring company in exchange for immediate cash, and that transaction often triggers a UCC filing.

The factoring company files a UCC-1 financing statement to publicly record its interest in the business’s receivables. This filing ensures that if the business defaults or faces financial trouble, the factoring company’s claim on those invoices takes priority over other creditors.

When a buyout occurs, it usually means a new lender or factoring company is paying off the existing factoring agreement to take over the claim. In that case, the original UCC filing is terminated or replaced by a new one, transferring the security interest from the old lender to the new party.

How UCC Filings Affect Factoring and Buyouts?

UCC filings play a big part in how factoring and buyout deals actually work behind the scenes. When a business sells its invoices to a factoring company, the factor files a UCC-1 to show it now has rights to those receivables.

That filing acts as public proof that the invoices are tied to the factoring agreement, keeping other lenders from claiming the same assets. In a buyout situation, the new factor or lender must first clear or replace the existing UCC filing before taking over, ensuring the transfer of rights is clean and legally sound.

Why UCC Filings Matter in Freight Factoring?

Protecting Ownership

A UCC filing secures the factor’s ownership of the invoices it buys. It ensures that no other lender or financial institution can claim those same receivables as collateral for another loan.

Preventing Double Financing

Many carriers work with multiple funding partners, which can create overlap in collateral. A UCC-1 filing prevents double financing by clearly identifying which factoring company holds the legal rights to the invoices.

Establishing Priority

When multiple creditors are involved, the UCC filing establishes who gets paid first. It gives the factoring company priority status, ensuring they are first in line to collect if the carrier defaults or files for bankruptcy.

Maintaining Transparency

A UCC filing provides full visibility into financial obligations. It lets other lenders know that specific invoices are already pledged, reducing confusion and keeping the factoring relationship open and transparent.

Building Trust

Properly filed UCC records build confidence between the carrier and the factoring company. Both parties understand their roles and rights, which helps maintain long-term, stable working relationships.

Simplifying Buyouts

When a carrier switches factoring companies, the existing UCC filing needs to be terminated or replaced. A clear filing history makes this process smoother, helping new factors quickly take over and continue funding without legal delays.

Supporting Business Growth

Consistent and accurate UCC filings strengthen a carrier’s financial credibility. Clean records show reliability, which makes it easier to secure better factoring terms or future financing opportunities.

Which Is the Best Freight Factoring Company In 2026?

Routiqo is the best overall freight factoring company in 2026, who need fast, reliable funding. It offers 1.5% rates, same-day payments, and no hidden fees, making it the most trusted choice for steady cash flow.

With fuel advances, free ELD devices, and 24/7 support, Routiqo keeps truckers on the road and financially secure. It’s built by trucking experts who understand what drivers need — simple, transparent, and fast factoring.

Leave a Reply