Key Takeaways:

- Spot, traditional, and selective factoring are the three main models businesses use to turn invoices into immediate cash.

- Spot factoring offers one-invoice flexibility, while traditional factoring provides steady long-term funding for consistent cash flow.

- Selective factoring lets businesses choose specific invoices to finance, giving them more control than traditional programs.

- The best factoring type depends on how often a business needs funding, how predictable its invoicing is, and how much flexibility it wants.

What Is Factoring?

Factoring is a financing method where a business sells its accounts receivable to a third-party company, known as a factor, in exchange for immediate cash. It helps companies smooth out cash-flow gaps by turning unpaid invoices into quick working capital.

The factor advances a portion of the invoice value upfront and releases the rest once the customer pays, minus a small fee. This arrangement allows businesses to keep operations running without waiting for long customer payment cycles.

How Does Factoring Work?

Factoring works by allowing a business to submit its customer invoices to a financing company that reviews their creditworthiness and payment reliability. Once the invoices are validated, the factor decides how much funding can be released based on the strength of the customer’s payment history.

After approval, the factor provides an advance that represents a portion of the invoice value, giving the business access to immediate funds without waiting for the normal payment timeline. This shift in cash availability helps companies handle operating costs or manage short-term needs more smoothly.

When the customer pays the invoice, the factor sends the remaining balance to the business after subtracting its service fee. This completes the cycle and enables the business to continue using factoring whenever additional cash-flow support is necessary.

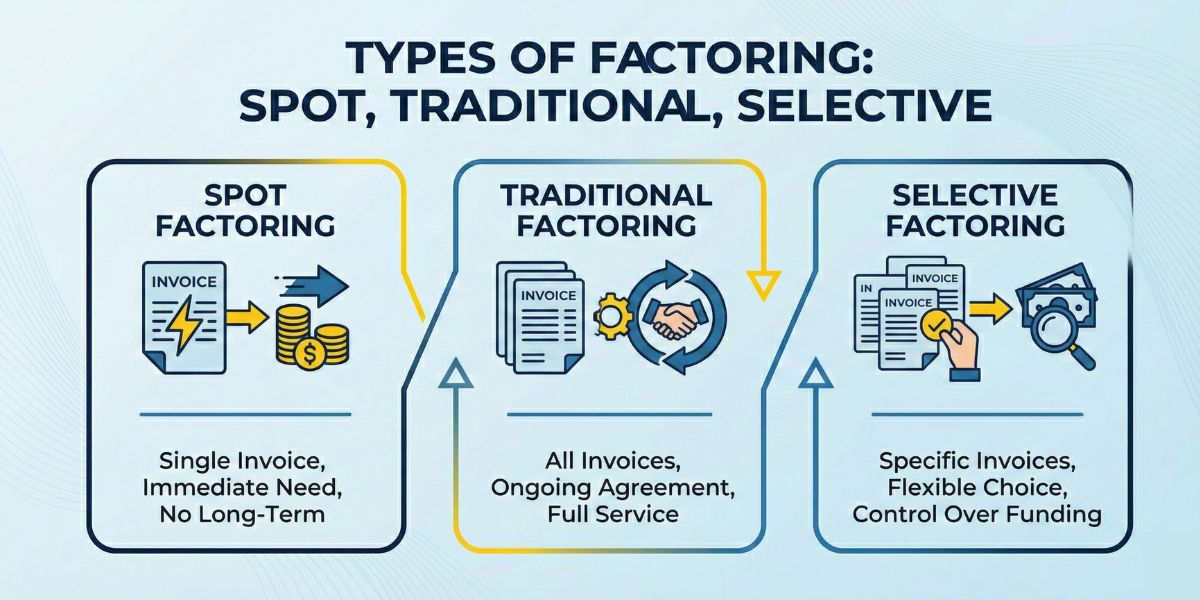

What Are The Main Types Of Factoring?

- Spot Factoring: Lets businesses fund a single invoice whenever they need quick cash without entering long-term agreements.

- Traditional Factoring: Provides ongoing funding through a committed contract where most or all invoices are factored each month.

- Selective Factoring: Allows companies to choose specific invoices or customers to fund, offering flexibility without full contract obligations.

What Is Spot Factoring?

Spot factoring is a short-term financing option where a business chooses a single invoice to convert into immediate cash. It is designed for companies that experience occasional cash-flow pressures and prefer a one-time solution instead of an ongoing arrangement.

This type of factoring is valued for its flexibility since it involves no long-term commitments or monthly volume requirements. Businesses often use it during seasonal slowdowns, unexpected expenses, or periods when only a small infusion of capital is needed.

How Does Spot Factoring Work?

- Invoice Selection: The business picks a single invoice that requires immediate funding. This step allows the company to target short-term cash needs without committing to multiple invoices.

- Submission to the Factor: The chosen invoice is sent to the factoring company for evaluation. The factor checks the invoice details and assesses the customer’s payment reliability.

- Approval and Advance: Once approved, the factor provides an upfront advance based on the invoice value. This gives the business quick access to working capital.

- Customer Payment Processing: The customer pays the invoice directly to the factor according to the original payment terms. This ensures smooth processing without additional steps for the business.

- Final Settlement: After receiving full payment, the factor releases the remaining balance to the business. A service fee is deducted, completing the transaction.

What Are The Pros & Cons Of Spot Factoring?

| Pros of Spot Factoring | Cons of Spot Factoring |

| Offers complete flexibility with no long-term contracts. | Higher fees compared to traditional factoring. |

| Ideal for occasional or seasonal cash-flow needs. | Each invoice requires individual review and approval. |

| Allows businesses to choose only the invoices they want to fund. | Limited scalability for companies needing frequent financing. |

| Quick access to working capital without monthly volume requirements. | May involve extra administrative or due-diligence charges. |

What Is Traditional Factoring?

Traditional factoring is a long-term financing arrangement where a business regularly sells most or all of its invoices to a factor. It is designed for companies with steady sales cycles that need predictable cash flow throughout the year.

This model relies on ongoing participation, meaning businesses submit invoices consistently rather than on an occasional basis. It is commonly used by companies that want dependable liquidity and are comfortable with structured agreements.

How Does Traditional Factoring Work?

- Monthly Invoice Submission: The business sends a steady flow of invoices to the factor as part of its ongoing agreement. This ensures predictable funding and supports continuous cash flow.

- Customer Credit Evaluation: The factor reviews the credit profiles of the business’s customers to determine eligible invoices. This step keeps risk under control and helps maintain consistent advance rates.

- Advance Disbursement: Approved invoices receive an upfront advance that covers a portion of their value. This advance gives the business immediate access to working capital.

- Collections Management: The factor takes over the responsibility of collecting payments from customers. This reduces administrative pressure and streamlines the payment process.

- Final Payout: After customer payments are received, the factor sends the remaining balance to the business. A standard service or discount fee is deducted to complete the transaction.

What Are The Pros & Cons Of Traditional Factoring?

| Pros of Traditional Factoring | Cons of Traditional Factoring |

| Provides steady and predictable cash flow for ongoing operations. | Requires long-term contracts with monthly volume commitments. |

| Offers lower fees due to consistent invoice submissions. | Limits flexibility for businesses with irregular sales cycles. |

| Reduces administrative workload through outsourced collections. | May involve credit requirements that exclude certain customers. |

| Strengthens cash-flow planning for growing companies. | Not ideal for businesses needing only occasional funding. |

What Is Selective Factoring?

Selective factoring is a financing option that lets a business choose the specific invoices it wants to fund. It suits companies that need occasional cash support but prefer to keep control over most of their receivables.

This approach works well for businesses with varying customer reliability or uneven cash-flow demands. It provides access to working capital without the obligation to factor every invoice on the books.

How Does Selective Factoring Work?

- Choosing Invoices: The business selects the invoices it wants to finance, focusing on customers or amounts that align with immediate cash needs.

- Submitting for Review: These selected invoices are sent to the factor, who checks the customer’s credit strength to confirm eligibility.

- Receiving the Advance: Once approved, the business receives an upfront advance based on the invoice value, giving it quick access to funds.

- Customer Payment: The customer pays the invoice directly to the factor following the original payment terms, keeping the process simple.

- Settling the Balance: After payment arrives, the factor returns the remaining amount to the business and deducts its fee to close the transaction.

What Are The Pros & Cons Of Selective Factoring?

| Pros of Selective Factoring | Cons of Selective Factoring |

| Lets businesses fund only the invoices they choose. | Can be more expensive than traditional factoring for frequent use. |

| Offers flexibility without committing to full-volume agreements. | Approval relies strongly on the credit quality of selected customers. |

| Helps manage cash flow for specific clients or short-term needs. | Not always ideal for companies needing continuous funding. |

| Allows greater control over which receivables are factored. | May involve minimum usage expectations depending on the provider. |

Key Differences Between Spot Factoring, Selective Factoring, And Traditional Factoring

Spot vs. Selective Factoring

Spot factoring is used when a business needs to fund just one invoice and move on. Selective factoring gives more room to choose several invoices as needed, making it easier to manage unpredictable cash-flow moments.

Spot vs. Traditional Factoring

Spot factoring keeps everything one-off and commitment-free, which is helpful for occasional needs but comes with higher costs. Traditional factoring works on routine submissions, creating steady cash flow and lowering fees over time.

Selective vs. Traditional Factoring

Selective factoring appeals to businesses that want control over which customers or projects they fund. Traditional factoring suits companies with consistent billing because it supports smooth, ongoing financing.

Flexibility Across All Three Models

Spot factoring offers the most flexibility since each invoice stands alone. Selective factoring provides choice without heavy commitments, while traditional factoring focuses on long-term stability.

Cost and Fee Considerations

Spot factoring usually costs more because every invoice is reviewed individually. Selective and traditional agreements tend to be more cost-friendly when invoices are submitted regularly.

Which Type Of Factoring Is Best For Small Businesses?

- Occasional Needs: Small businesses that only face cash gaps once in a while usually benefit most from spot factoring. It gives them quick access to funds without committing to any ongoing program.

- Selective Control: Companies with customers who vary in reliability often choose selective factoring. It allows them to finance only the invoices they trust while keeping the rest in-house.

- Steady Funding: Traditional factoring works best for businesses with consistent billing and predictable cash flow. Lower fees and routine advances make it easier for them to plan month to month.

- Seasonal Cycles: Businesses that experience slow periods during certain times of the year lean toward spot or selective factoring. These options support short-term needs without locking them into long-term contracts.

- Growing Operations: Companies increasing their invoice volume usually see more value in traditional factoring. As activity rises, steady funding helps support expansion and reduces financial strain.

What Should Businesses Consider Before Choosing A Factoring Type?

Cash-Flow Timing Needs

Companies with irregular cash shortages benefit from spot or selective models. Daily operating demands may require the consistency of traditional factoring.

Invoice Volume and Customer Credit Quality

Large or steady invoice volumes favor traditional agreements. Mixed customer credit quality aligns well with selective or spot factoring.

Contract vs. No-Contract Preference

Spot factoring avoids long-term commitments entirely. Traditional models lock in stability with contract-based structures.

Industry Requirements

Industries with seasonal demand may rely on spot factoring. Manufacturers and exporters with consistent billing often use traditional agreements.

Conclusion

Factoring comes in several forms, and each type offers its own balance of flexibility, cost, and commitment. Spot, selective, and traditional factoring all solve cash-flow challenges, but they support businesses differently depending on how often funding is needed and how predictable their invoicing patterns are.

Small businesses can choose the model that fits their rhythm rather than adjusting their operations to a financing structure. Whether they need one-time support, selective control, or steady long-term funding, understanding these options makes it easier to manage working capital and maintain financial stability.

Leave a Reply