Key Takeaways:

- Recourse factoring helps businesses access quick and affordable funding while keeping the responsibility for unpaid invoices with the seller.

- Non-recourse factoring shifts the credit risk to the factor, giving businesses protection against customer insolvency or default.

- The core difference lies in how each model manages risk, cost, and payment security for the business.

- The right choice depends on customer reliability, cash flow needs, and how much risk a business is willing to carry.

What Is Recourse Factoring?

Recourse factoring allows a business to receive quick cash by selling its invoices while still being responsible if customers fail to pay. The factor provides the funds but not the protection against unpaid debts, keeping the credit risk with the business.

This method usually comes with lower fees and higher advance rates because the factor carries minimal risk. Businesses often receive between 80–95% of the invoice value upfront, making it a cost-effective way to strengthen cash flow.

For example, a manufacturer might sell a $100,000 invoice and get $90,000 immediately from the factor. If the customer pays, the manufacturer collects the remaining balance minus a small fee; if not, the manufacturer must repay the $90,000.

What Are The Advantages & Disadvantages Of Recourse Factoring?

Advantages

- Lower Cost: The factor charges less because the business carries the credit risk. This makes it one of the most affordable financing methods for steady cash flow.

- Higher Cash Advance: Companies often receive 80–95% of their invoice value upfront, which keeps operations moving smoothly.

- Quick Turnaround: Funds are usually released within one to two days, ideal for covering payroll or supplier payments.

- Easier to Qualify: Lenders focus more on your company’s performance than the customer’s credit score, speeding up approvals.

- Direct Customer Contact: You keep managing your clients, which helps preserve business relationships and reputation.

Disadvantages

- Full Responsibility for Non-Payment: If an invoice goes bad, you have to buy it back or reimburse the factor.

- Risk of Bad Debts: One major default can quickly cut into profits and disrupt cash flow.

- Repayment Pressure: When customers pay late, it can squeeze your finances and affect regular operations.

- No Risk Shield: The factor won’t protect you from losses if your client becomes insolvent or disputes the invoice.

- Accounting Impact: Because you retain liability, invoices may stay on your books as debt, influencing your balance sheet.

When To Choose Recourse Factoring?

Recourse factoring fits businesses that:

- Work with financially stable clients with a long payment history.

- Require quick cash access at minimal cost.

- Have strong internal credit control and can handle occasional defaults.

Example:

A logistics company with long-term corporate contracts uses recourse factoring to speed up cash flow while retaining confidence in customer payments.

What Is Non-Recourse Factoring?

Non-recourse factoring allows a business to hand over the credit risk to the factor instead of keeping it in-house. If a customer goes bankrupt or becomes insolvent, the factor absorbs the loss, protecting the business from bad debt.

This type of agreement comes with higher fees because the factor takes on more risk. Before approval, factors usually review each debtor’s credit history carefully to make sure the invoices are secure.

For example, a staffing company might sell a $50,000 invoice under a non-recourse agreement. If the client cannot pay, the factor covers the loss, giving the business peace of mind in exchange for a slightly higher cost.

What Are The Advantages & Disadvantages Of Non-Recourse Factoring?

Advantages

- Credit Risk Protection: The factor takes on the responsibility for unpaid invoices if the customer becomes insolvent, reducing financial stress for the business.

- Stable Cash Flow: Businesses receive immediate funds without worrying about potential bad debts, keeping operations consistent.

- Improved Balance Sheet: Since the factor assumes the risk, some invoices may be removed from the company’s liabilities, improving financial ratios.

- Professional Credit Control: Factors conduct thorough credit checks and manage collections, saving time and reducing administrative work.

- Peace of Mind: Knowing that invoice payments are secured allows owners to focus on business growth rather than chasing overdue accounts.

Disadvantages

- Higher Fees: The factor charges more to cover the additional risk, which can reduce overall profit margins.

- Lower Advance Rates: Companies usually receive between 70–90% of the invoice value upfront, slightly less than in recourse agreements.

- Strict Approval Process: Factors carefully evaluate each customer’s creditworthiness before accepting invoices, which can limit eligibility.

- Partial Coverage: Most non-recourse contracts only cover non-payment caused by insolvency, not disputes or delayed payments.

- Reduced Flexibility: Businesses have to work within the factor’s credit policies, which may restrict which clients or invoices can be funded.

When To Choose Non-Recourse Factoring?

Non-recourse factoring fits businesses that:

- Serve unfamiliar or high-risk clients.

- Want to transfer credit risk and ensure predictable revenue.

- Prefer outsourced collections and risk monitoring.

Example:

A construction supplier serving multiple new clients uses non-recourse factoring to safeguard cash flow against potential non-payment from new accounts.

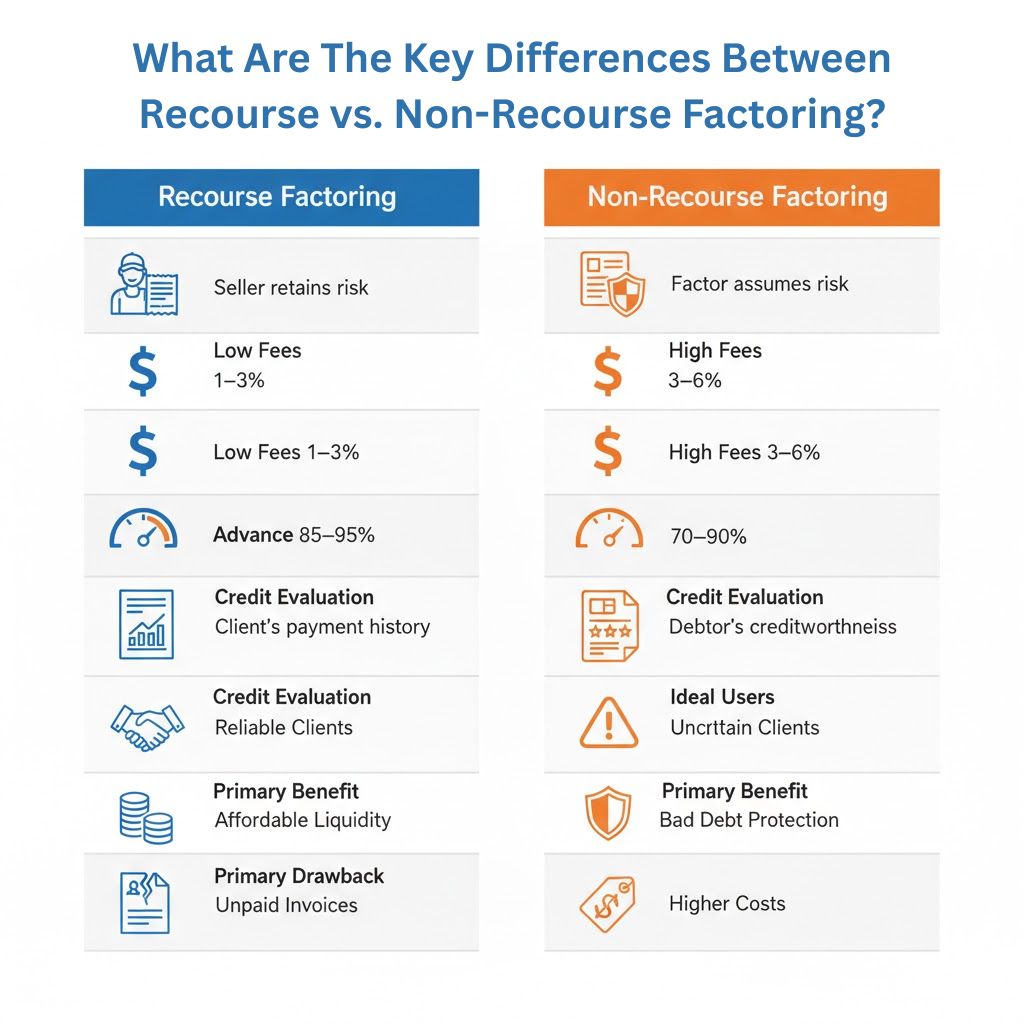

What Are The Key Differences Between Recourse vs. Non-Recourse Factoring?

| Aspect | Recourse Factoring | Non-Recourse Factoring |

| Risk Responsibility | Seller retains risk of non-payment. | Factor assumes risk of approved non-payment. |

| Cost Structure | Lower fees, around 1–3% of invoice value. | Higher fees, around 3–6% of invoice value. |

| Advance Rate | Higher advances, typically 85–95%. | Lower advances, typically 70–90%. |

| Credit Evaluation | Focus on seller’s business health. | Focus on debtor’s credit rating. |

| Ideal Users | Businesses with reliable customers. | Businesses exposed to higher credit risk. |

| Primary Benefit | Cheaper liquidity solution. | Strong protection against bad debts. |

| Primary Drawback | Exposure to unpaid invoices. | Higher cost and selective approval. |

How To Choose The Right Model For Your Business?

Check Customer Reliability

Start by looking at how your customers handle payments. If most pay on time, recourse factoring works well; if delays or defaults are common, non-recourse factoring offers better protection.

Know Your Risk Comfort

Be clear about how much risk you can handle. Businesses that can absorb a few late payments usually prefer recourse factoring, while those that want stability often go for non-recourse.

Balance Cost and Security

Lower fees sound attractive, but they come with higher responsibility. Recourse factoring is more affordable, while non-recourse gives you security when a customer can’t pay.

Review Your Cash Flow Needs

Think about how quickly you need working capital. Recourse factoring delivers funds faster, while non-recourse offers steady income even when clients face financial trouble.

Read the Fine Print

Understand exactly what’s covered in your factoring agreement. Some non-recourse contracts only protect against insolvency, while others include a wider range of risks.

Consider Your Industry

Different industries face different payment challenges. Companies in stable sectors like manufacturing often use recourse factoring, while those in staffing or construction lean toward non-recourse for extra security.

Plan for the Future

Your choice should match where your business is heading. Recourse factoring supports short-term growth, while non-recourse becomes valuable as you scale and take on bigger or riskier clients.

Talk to an Expert

If you’re unsure, seek professional guidance. A financial advisor or factoring specialist can help you compare both models and choose what aligns best with your goals.

The Top Factoring Company You Should Choose

Routiqo Freight Factoring helps owner-operators and small trucking businesses get paid faster without worrying about long waits or hidden fees. With simple online applications and funding in less than 24 hours, it keeps cash flowing smoothly between loads.

The service is built specifically for truckers, offering competitive rates starting at 1.5% and complete transparency with no surprise charges. Each client gets a dedicated account manager, ensuring personal support and real communication instead of automated systems.

Beyond quick payments, Routiqo provides real value through tools like free ELD devices, fuel advance programs, and 24/7 customer assistance. It’s a reliable, trucker-focused solution that combines speed, security, and personal service to keep drivers on the road and financially confident.

Leave a Reply