Key Takeaways:

- Exiting a factoring contract requires careful review of terms, fees, and notice periods to avoid unexpected costs or legal issues.

- Maintaining accurate records, reconciling balances, and confirming lien releases ensures a clean and dispute-free closure.

- Planning alternative financing before termination helps preserve cash flow and operational stability during the transition.

- A thoughtful, well-timed exit strengthens financial control and positions the business for sustainable, long-term growth.

What Is a Factoring Contract?

A factoring contract is a financial arrangement between a business and a factoring company, often called a factor. It allows the business to sell its accounts receivable in exchange for quick cash, usually between 70% and 90% of the invoice value.

The agreement clearly defines the term length, fees, and conditions for ending or renewing the partnership. It also establishes ownership rights, detailing who manages the receivables ledger and how customer payments are handled.

In the United States, most factors protect their interest by filing a UCC-1 lien against the receivables they purchase. Exiting such a contract without proper notice or settlement can create serious legal and financial complications for the business.

Why Do Businesses Exit Factoring Contracts?

- High factoring costs: Over time, fees and discount rates can eat into profits. As a business’s credit improves, traditional financing often becomes more affordable than factoring.

- Poor service experience: Delayed funding, miscommunication, or aggressive collection practices from the factor can strain customer relationships and disrupt operations.

- Improved cash flow stability: When regular customer payments increase and reserves grow, many companies no longer need to rely on advances from a factoring company.

- Switching to alternative funding: Businesses often move to lines of credit, bank loans, or invoice discounting for more flexibility and lower costs.

- Avoiding automatic renewals: Some contracts renew without clear notice, locking businesses in for another term. Proactive termination helps them regain control over their financing.

- Change in business model: Companies that shift from credit-based sales to upfront payment structures often find factoring unnecessary and costly to maintain.

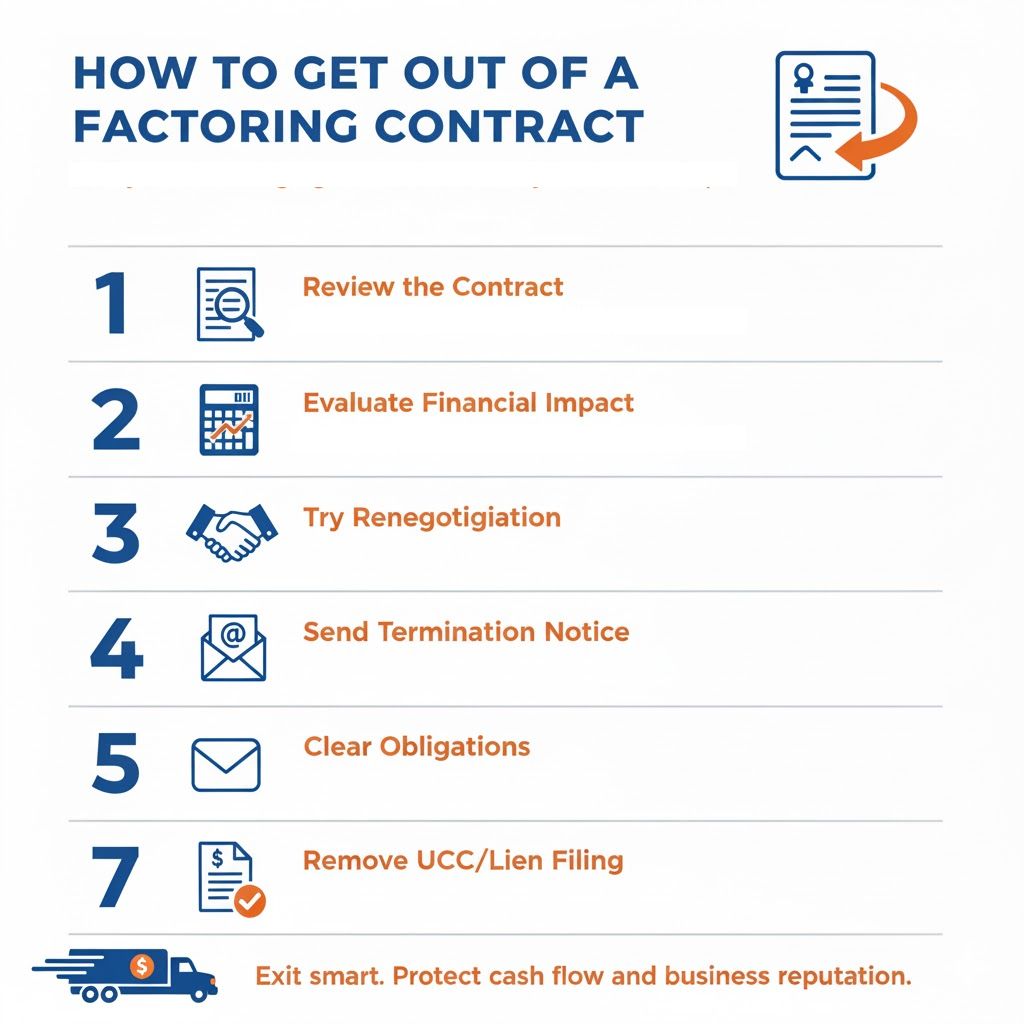

How to Get Out of a Factoring Contract?

Exiting a factoring contract requires clarity, proper timing, and compliance with your agreement. The goal is to end the relationship smoothly without financial or legal setbacks.

Step 1: Review the Contract Thoroughly

Begin by carefully reviewing your signed factoring agreement. Focus on the following key clauses:

- Minimum term: The duration you are legally bound to the factor.

- Notice period: Usually 30–90 days before renewal or expiration.

- Termination procedure: Specifies how notice must be delivered—email, letter, or certified mail.

- Early exit fees: Some contracts charge 2–5% of the annual factoring volume for early termination.

- Renewal clause: Many agreements renew automatically if notice is not given on time.

Understanding these clauses helps you avoid disputes and unexpected costs.

Step 2: Evaluate the Financial Impact

Leaving early has financial consequences. Calculate the real cost before giving notice:

- Outstanding advances: Amount already paid by the factor but not yet repaid.

- Reserve balance: Money held for invoices that remain unpaid.

- Termination fee: Flat charge or percentage of your projected volume.

- Buyout value: Total balance if another factoring company takes over.

For example, a $100,000 monthly volume with a 2% early termination fee equals $12,000 in cost if you leave six months early. A clear cash-flow forecast keeps your business stable during the transition.

Step 3: Discuss Renegotiation Before Exiting

Before canceling, speak directly with your factor. Many issues resolve through negotiation. You can request:

- A lower discount rate or improved fee structure.

- A shorter advance hold period for faster access to funds.

- A switch to spot factoring, handling only select invoices.

- A transition from recourse to non-recourse terms.

Most factoring companies prefer retaining clients and will adjust terms if communication is professional and timely.

Step 4: Send a Formal Termination Notice

Once you decide to leave, send a written notice that matches the contract requirements. Include:

- Your business name and account number.

- The contract section that permits termination.

- The effective termination date.

- A request for lien release (UCC filing).

Step 5: Clear All Outstanding Obligations

After notice, close all remaining balances.

- Pay any unsettled invoices or advance differences.

- Allow the factor to collect payments for invoices already sold.

- Request a final reconciliation showing reserves and deductions.

- Obtain a release letter confirming the account is fully settled.

This document protects your business from future claims and enables new funding opportunities.

Step 6: Remove UCC or Lien Filings

In the U.S., most factors file a UCC-1 financing statement to claim security over receivables. Once the contract ends, they must file a UCC-3 termination to cancel that claim.

Always ask for a copy of the lien release and verify it through your state’s UCC database. Without it, new lenders will see your receivables as encumbered assets.

Step 7: Transition to a New Funding Source

Maintain steady cash flow after termination by preparing your next financial move. Common alternatives include:

- Invoice discounting: Offers funding without giving up control of collections.

- Business line of credit: Suitable for stable credit profiles.

- Asset-based lending: Secured by receivables or inventory.

If switching to another factoring provider, coordinate a buyout agreement between both companies to ensure a smooth transition for your customers.

Common Challenges During Factoring Contract Exit

| Challenge | Impact | Solution |

| Auto-renewal clause | Extends contract unintentionally | Mark renewal date on calendar and give early notice |

| Early termination fees | Reduces cash flow | Negotiate fee reduction or credit against future business |

| Uncollected invoices | Factor retains funds | Reconcile aging report with factor |

| UCC filing remains | Blocks new financing | Obtain UCC-3 termination |

| Poor communication | Delays closure | Communicate in writing and maintain records |

What are the Best Practices for a Clean Exit From Factoring Contract?

Document Everything

Keep every piece of communication related to your factoring agreement. Save emails, letters, statements, and signed copies of notices in one place. Having accurate records makes it easier to handle questions later and helps you prove that each step of the exit followed the correct process.

Reconcile Balances Early

Check your figures before the contract officially ends. Compare your internal records with the factor’s statements to ensure every invoice, reserve amount, and payment aligns. Early reconciliation helps prevent confusion, delays, or disputes once the relationship ends.

Use Professional Advice

Seek guidance from a financial advisor or attorney familiar with factoring agreements. They can review the contract, explain any complex clauses, and make sure your exit follows the legal requirements. Professional advice adds an extra layer of protection for your business.

Plan Cash-Flow Continuity

When factoring stops, the steady flow of advances usually stops too. Make arrangements for another source of funding at least a few weeks before your contract ends. Securing a line of credit or using invoice discounting helps your business stay financially stable during the transition period.

Confirm Lien Release

After the final payment and reconciliation, ask the factoring company to remove any UCC-1 lien from your receivables. Request written proof of release and verify it through your state’s online database. Until that lien is cleared, most lenders will view your receivables as restricted assets.

In Closing

A clean exit from a factoring contract is about closing every loop with accuracy and professionalism. When you document your actions, confirm your numbers, seek expert advice, plan for cash continuity, and secure lien release, you protect your company from unnecessary risk and move forward with financial confidence.

When Not to Exit?

High Termination Costs

If the termination fee exceeds the projected savings from exit, maintaining the contract remains financially logical. Early termination in such cases reduces liquidity and creates unnecessary expense.

Dependence on Factoring Advances

If the business relies on factoring to maintain daily cash flow, exiting can interrupt financial stability. Retaining the contract ensures consistent access to working capital until a reliable replacement is secured.

Unfavorable Market Conditions

When credit markets are tight and lending standards are restrictive, alternate financing options may not be available. Continuing with the existing factoring arrangement sustains operational funding during such conditions.

Strong Relationship with Factor

If the current factoring company provides fast funding, transparent reporting, and reliable customer support, maintaining the relationship is beneficial. Stable service and predictable terms increase operational efficiency.

Upcoming Contract Expiration

If the contract is close to its natural end date, early exit serves no strategic advantage. Waiting until the formal expiration avoids penalty charges and simplifies the transition process.

Example Timeline for Contract Exit

| Time Frame | Action |

| Day 1 | Review the contract and identify renewal date |

| Day 10 | Evaluate costs and cash-flow impact |

| Day 15 | Discuss renegotiation options with factor |

| Day 30 | Send termination notice |

| Day 60 | Confirm receipt and settle outstanding invoices |

| Day 75 | Obtain release letter and lien termination |

| Day 90 | Begin with new financing partner |

Legal Considerations

Factoring contracts are legally binding financial agreements that outline the rights and obligations of both parties. Each clause carries specific consequences if it is breached or misunderstood.

When reviewing your contract, pay attention to the governing law and jurisdiction sections. These determine where any legal disputes will be resolved and which state or country’s laws apply.

It’s also important to verify how invoice ownership transfers once factoring begins. Once invoices are sold, they become the property of the factoring company until all contractual terms are fulfilled.

Conclusion

Exiting a factoring contract is a careful process that requires attention to detail and clear communication. When handled correctly, it allows a business to move forward with stronger control over its cash flow and financial choices.

A well-planned exit is less about ending a partnership and more about creating stability for future growth. By staying organized and following each step with intention, a company can leave the agreement smoothly and build a healthier financial foundation.

Leave a Reply