Key Takeaway:

- Advance rate defines how much cash a business can access immediately based on its collateral value, directly influencing short-term liquidity.

- Reserve represents the portion of funds held back by the lender, affecting the timing and consistency of cash inflows.

- A balanced relationship between advance rate and reserve ensures steady working capital, stable operations, and reduced financial stress.

- Optimizing both elements through strong collateral, reliable customers, and smart negotiation strengthens cash flow and long-term financial flexibility.

What Is Advance Rate?

Advance rate is the percentage of a collateral’s value that a lender provides as a loan. It defines the immediate cash a business receives based on the collateral’s assessed worth.

Formula: Advance Rate = (Loan Amount ÷ Collateral Value) × 100

For example, if a company pledges $500,000 in eligible invoices and the lender offers an 80% advance rate, the lender advances $400,000 immediately.

Key Factors That Influence the Advance Rate

- Type of Collateral: Lenders give higher advance rates for liquid assets like invoices or cash deposits. Receivables from reputable buyers receive 80-90%, while inventory or equipment often receives 50-70%.

- Borrower Credit Quality: Businesses with strong credit and consistent payment histories receive higher advance rates.

- Customer Creditworthiness: For invoice factoring, the reliability of end customers determines the risk profile and, consequently, the advance rate.

- Industry Volatility: Stable industries such as healthcare or logistics often receive higher advance percentages compared to high-risk sectors such as construction or retail.

- Macroeconomic Conditions: In periods of economic uncertainty, lenders lower advance rates to protect their exposure.

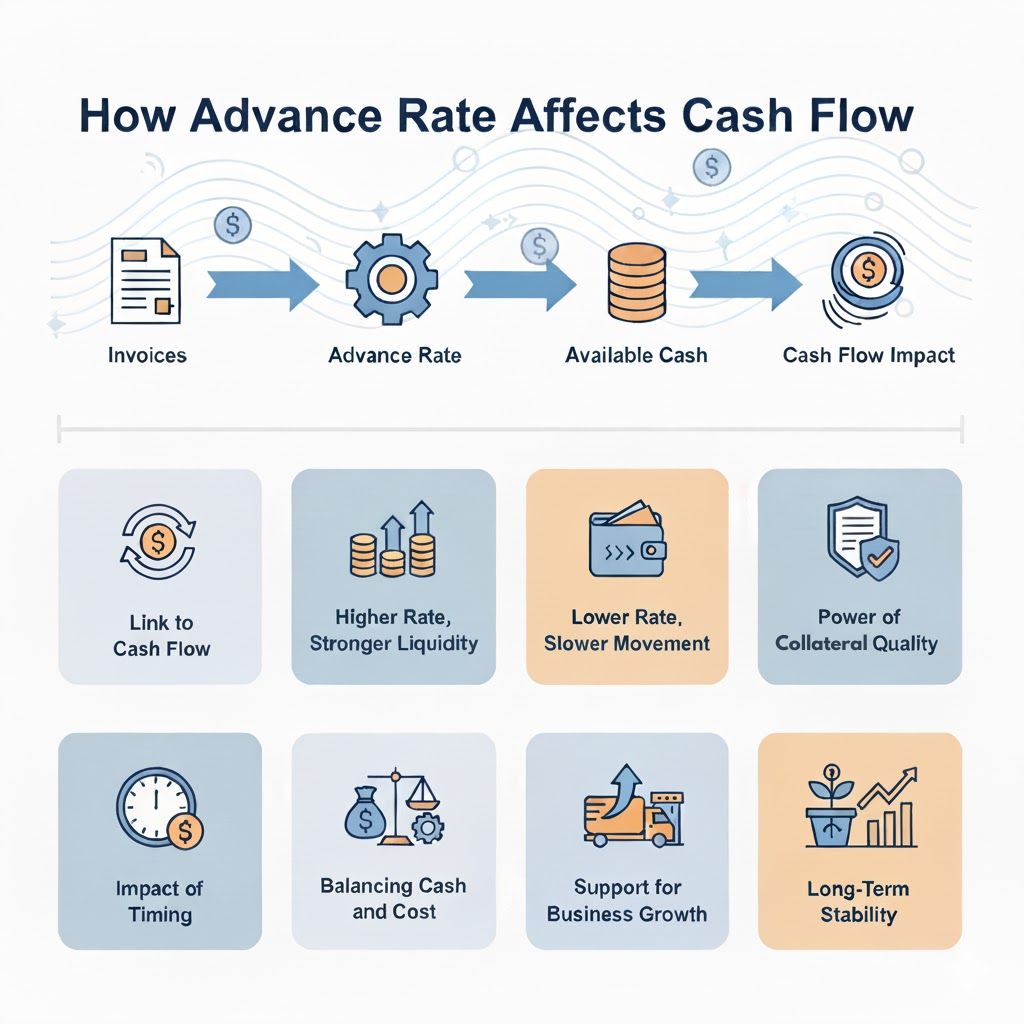

How Advance Rate Affects Cash Flow?

Link to Cash Flow

The advance rate directly shapes your cash flow because it controls the amount you get right away. A higher rate means quicker funds to cover your operating needs.

Higher Rate, Stronger Liquidity

When the advance rate goes up, more cash becomes available for daily use. This gives your business the flexibility to manage expenses without waiting for payments.

Lower Rate, Slower Movement

A lower advance rate reduces the amount of money you receive instantly. That slower movement of cash can create tight spots in your working capital.

Power of Collateral Quality

The better your collateral, the higher your advance rate tends to be. Reliable invoices or assets make lenders confident, improving your cash flow access.

Impact of Timing

The speed at which funds are advanced changes how steady your cash feels. Quick advances help maintain flow, while delays create unwanted pressure.

Balancing Cash and Cost

A high advance rate boosts liquidity but can come with higher fees. Finding the right balance ensures your cash flow stays strong without eating into profits.

Support for Business Growth

A healthy advance rate keeps your operations fueled and flexible. It lets you restock inventory, pay staff, and invest in growth when opportunities arise.

Long-Term Stability

Tracking and managing your advance rate protects your long-term financial rhythm. It keeps your cash flow reliable even when business conditions shift.

What Is Reserve?

Reserve is the portion of the collateral value withheld by the lender until the borrower’s customer pays or until certain conditions are met.

In invoice factoring and asset-based lending, the lender retains a percentage as a cushion against disputes, chargebacks, or non-payment risk.

Formula: Reserve = Collateral Value – Advanced Amount

For instance, with invoices worth $500,000 and an advance rate of 80%, the reserve equals $100,000. The factor releases this $100,000 (less fees) when customers pay their invoices in full.

What Are the Common Reserve Percentages?

Common reserve percentages depend on how risky a business or industry is. Companies with steady customers and reliable payments usually see lower reserves, while those with unpredictable cash cycles face higher holdbacks.

Low-risk industries often keep reserves between 5–10%, moderate-risk industries range around 10–20%, and high-risk industries can go as high as 20–40%. These differences reflect factors like payment delays, customer disputes, and the overall credit strength of the business.

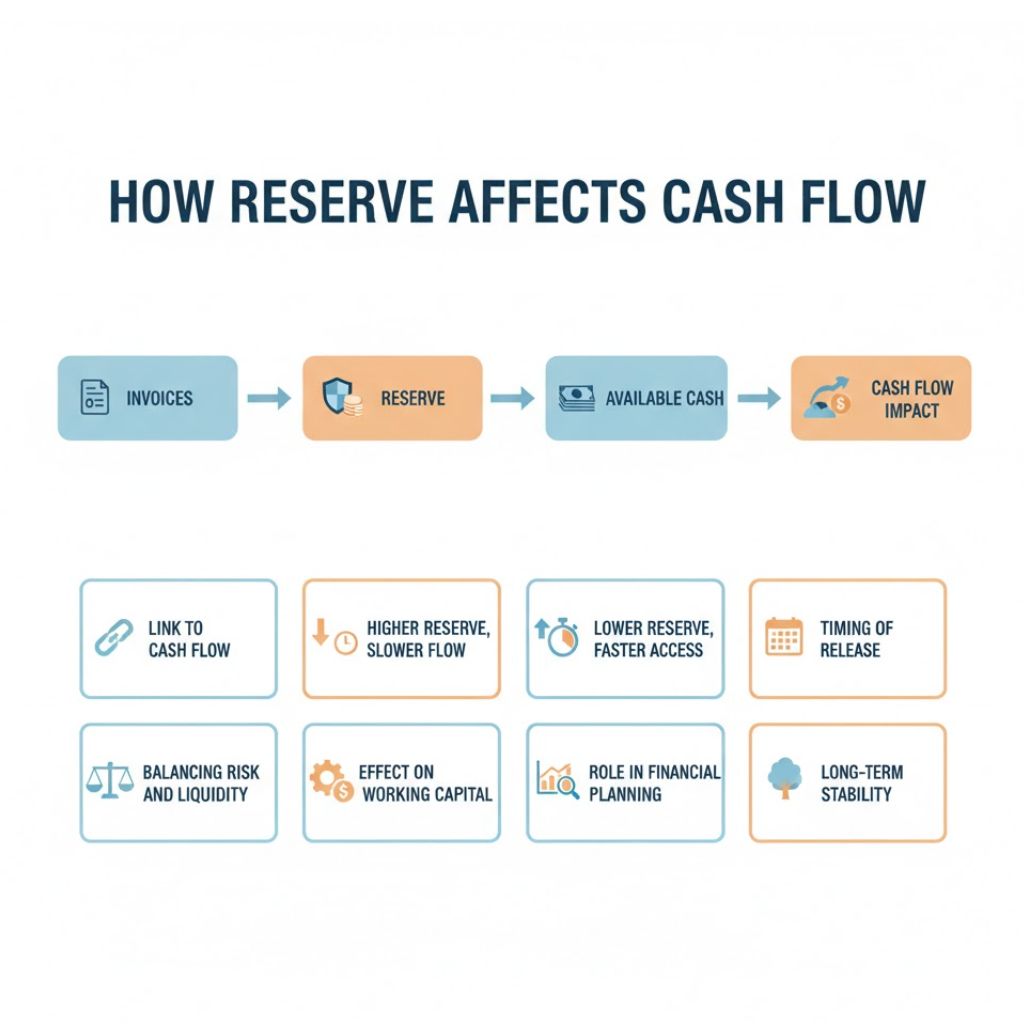

How Reserve Affects Cash Flow?

Link to Cash Flow

The reserve directly influences how much cash you get immediately after funding. A larger reserve means less upfront cash and slower liquidity.

Higher Reserve, Slower Flow

When the reserve percentage increases, more money stays on hold. This can make it harder to cover short-term expenses or manage daily operations.

Lower Reserve, Faster Access

A smaller reserve lets you receive a greater share of your funds right away. It speeds up your cash flow and gives you more flexibility to handle business costs.

Timing of Release

Cash flow improves once the reserve is released after customer payments are collected. The faster those payments come in, the sooner your business regains that held-back cash.

Balancing Risk and Liquidity

The reserve keeps lenders safe while giving you room to borrow confidently. Managing the balance between risk protection and liquidity ensures a smooth financial cycle.

Effect on Working Capital

Reserves tie up a portion of your working capital temporarily. Predicting when those reserves will be released helps keep your operations funded and consistent.

Role in Financial Planning

Knowing your reserve amount helps you plan more precisely. It allows you to forecast cash inflows and schedule spending without running into sudden shortages.

Long-Term Stability

Well-managed reserves bring stability to your financing relationship. They help maintain trust with lenders while keeping your cash flow predictable over time.

What Is the Relationship Between Advance Rate and Reserve?

Advance rate and reserve are two sides of the same transaction. Together, they determine the percentage of working capital available now versus later.

Total = Advance + Reserve = 100% of Collateral Value

If a lender offers an advance rate of 80%, the implied reserve equals 20%.

If the advance rate rises to 85%, the reserve drops to 15%.

Their relationship defines cash-flow flexibility:

- A higher advance rate reduces reserve, improving immediate cash flow.

- A higher reserve delays cash flow, but provides lender protection and better financing stability over time.

Example of Cash Flow Impact

Scenario 1:

- Collateral Value: $1,000,000

- Advance Rate: 80%

- Reserve: 20%

- Immediate Cash: $800,000

- Reserve Release: $200,000 (after invoice collection)

Scenario 2:

- Collateral Value: $1,000,000

- Advance Rate: 90%

- Reserve: 10%

- Immediate Cash: $900,000

- Reserve Release: $100,000

The difference of $100,000 in immediate funding improves liquidity, speeds up purchasing power, and strengthens short-term cash-flow capacity.

How Advance Rate & Reserve Influence Working Capital?

Liquidity Access

Higher advance rates increase the proportion of assets converted into cash. This liquidity supports inventory purchases, payroll, and operational expansion.

Operational Flexibility

Businesses with predictable reserve releases maintain more accurate cash-flow forecasting. Consistent release schedules improve decision-making on expenses and investments.

Cost Implications

High advance rates usually come with higher interest or factoring fees. Businesses must evaluate whether the cost of liquidity justifies the cash-flow benefit.

Risk Management

The reserve protects lenders from potential losses. This structure makes financing accessible to companies with weaker balance sheets or limited credit history.

Optimizing Advance Rate and Reserve for Better Cash Flow

Improve Collateral Quality

Maintain accurate, up-to-date receivables and ensure customers have strong payment histories. Clean receivables data increases advance rates.

Strengthen Customer Credit Screening

Financing companies evaluate end customers when determining advance percentages. Selling to reliable buyers improves overall advance limits.

Negotiate Favorable Terms

Businesses with consistent turnover and low delinquencies can negotiate higher advance rates and lower reserve requirements.

Monitor Payment Cycles

Reserve release depends on invoice payment. Fast-paying customers shorten the reserve release window, accelerating cash inflows.

Use Real-Time Cash-Flow Forecasting

Project cash inflows including reserve releases. Track daily positions and plan expenditures based on verified reserve release timelines.

Balance Cost and Liquidity

Do not pursue the highest possible advance rate if it leads to excessive fees. Optimal liquidity occurs where working-capital benefit outweighs financing cost.

Common Pitfalls

Overestimating Cash Availability

Businesses sometimes plan spending based solely on the advance amount, ignoring reserve delays. This mismatch creates liquidity shortfalls.

Neglecting Reserve Timing

Even with a strong advance rate, delayed reserve release can interrupt cash cycles. Payment-term forecasting must align with reserve schedules.

Misunderstanding Effective Cost

Factoring fees, interest, and administrative charges reduce the actual value of reserves released. Always calculate net cash flow, not gross values.

Ignoring Collateral Deterioration

If receivables age beyond eligibility limits, lenders can reduce the advance rate or hold additional reserves, tightening liquidity mid-cycle.

Practical Example

A manufacturing firm generates $2 million in monthly invoices. Its factor offers an 85% advance rate and a 15% reserve.

- Immediate cash = $1.7 million

- Reserve = $300,000

- Reserve release occurs after customers pay in 45 days.

If the firm negotiates a 90% advance rate and 10% reserve, immediate cash rises to $1.8 million — a $100,000 improvement in working capital. Over a year, that equates to $1.2 million in additional liquidity, enough to finance inventory expansion without new debt.

Conclusion

A well-structured advance rate and reserve setup keeps your cash flow steady and predictable. When both are managed with balance, your business gains the liquidity it needs today while maintaining the financial security required for tomorrow.

Understanding how these two elements work together helps you make smarter financing decisions and avoid cash shortages. With the right mix of advance rate and reserve, your business can stay flexible, fund growth confidently, and build a stronger financial foundation over time.

Leave a Reply