What Is Factoring?

Factoring is a financial solution where a business sells its accounts receivable to a factoring company for immediate funding. The factor advances a percentage of the invoice amount and releases the remainder after the customer pays.

This arrangement eliminates long waiting periods caused by slow-paying customers. It helps companies cover payroll, fuel, supplies, and operating expenses without relying on traditional loans.

For example, a freight carrier with 30–60 day customer terms can use factoring to receive same-day funding, ensuring continuous operations.

Who Are the Main Parties in Factoring?

Client (Business Selling Invoices)

The client is the business that generates invoices for goods or services delivered. It sells these invoices to a factor to access faster working capital.

Account Debtor (Customer Owing Payment)

The account debtor is the customer responsible for paying the invoice. Their credit profile determines whether the factor accepts the invoice for funding.

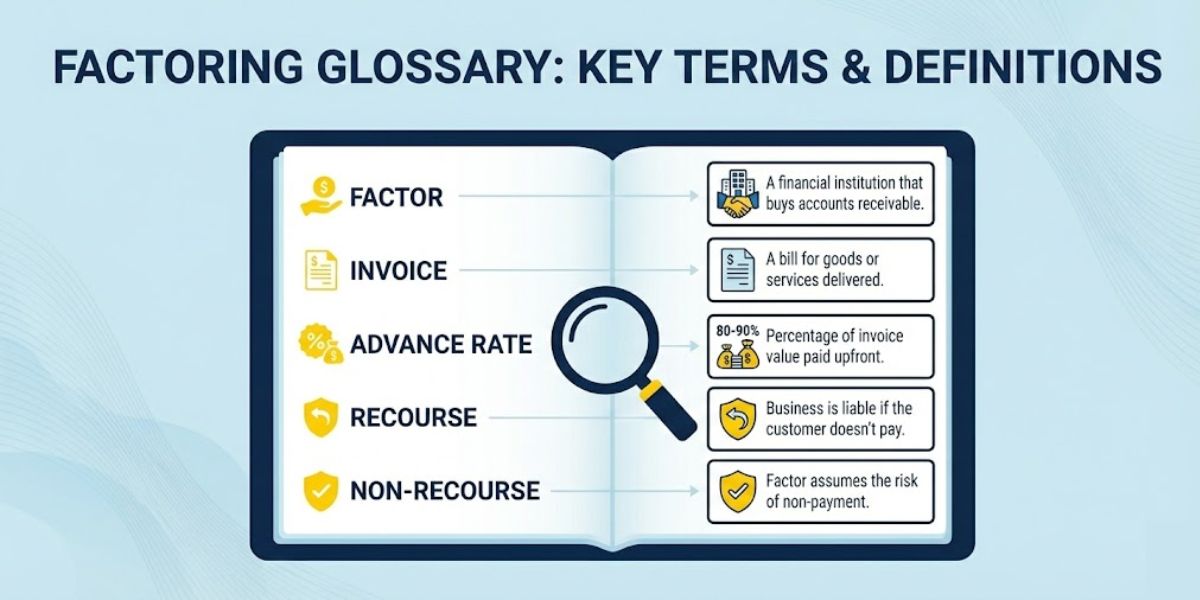

Factor (Factoring Company)

The factor purchases invoices at a discount and provides upfront cash to the client. It manages the collection process and returns the reserve once payment is received.

Now that the main participants are clear, let’s examine the key financial terms used throughout factoring arrangements.

What Are the Key Financial Terms Used in Factoring?

Advance Rate

The advance rate is the percentage of the invoice value paid upfront by the factor. It usually ranges from 70% to 95%, depending on industry risk and customer payment history.

Reserve / Holdback

The reserve is the remaining percentage of the invoice held until the customer pays. After payment, the factor releases it minus applicable fees.

Factoring Fee / Discount Rate

The factoring fee is the cost charged for purchasing the invoice and handling payment collection. It is typically expressed as a percentage per week or month until the customer pays.

Accounts Receivable Aging Report

An aging report organizes unpaid invoices by the number of days outstanding. Factors use it to evaluate risk and determine which invoices qualify for funding.

Debt Financing

Debt financing involves borrowing money and repaying it with interest. Unlike factoring, it adds liabilities to the balance sheet because it is a loan, not a sale of assets.

Rebate

A rebate is a credit or refund given back to the client when certain conditions, such as early customer payment, are met. It reduces overall factoring costs.

Dilution

Dilution refers to any reduction in the expected invoice value, including disputes, returns, or short payments. High dilution signals elevated risk for factoring companies.

Chargeback

A chargeback occurs when an invoice is returned to the client because the customer does not pay within the agreed time frame. This typically happens in recourse factoring arrangements.

Reserve Release

Reserve release is the moment the held-back portion of the invoice is returned once payment is collected. It finalizes the funding cycle.

These financial terms influence pricing, risk, and cash flow, making them critical for understanding any factoring contract.

What Are the Different Types of Factoring Arrangements?

Recourse Factoring

Recourse factoring requires the client to repay the factor if the customer does not pay. Because the client retains the credit risk, fees are usually lower.

Non-Recourse Factoring

Non-recourse factoring shifts the risk of customer nonpayment to the factor. This option offers more protection but comes with higher fees and stricter credit standards.

Spot Factoring / Single-Invoice Factoring

Spot factoring allows a business to factor individual invoices without lengthy commitments. It offers flexibility for companies with occasional cash-flow needs.

International / Cross-Border Factoring

Cross-border factoring supports companies that invoice customers in other countries. It helps manage currency, political, and payment risks in global trade.

These models show how factoring can adapt to different levels of risk and funding needs.

How Does the Factoring Process Work?

Factoring begins when a business submits an invoice to a factor for approval. The factor verifies the invoice and issues the advance payment.

Once the customer pays, the factor deducts fees and releases the remaining reserve. This creates predictable cash flow even when customers have long payment terms.

A staffing agency, for example, can factor its invoices weekly to ensure payroll funds arrive on time despite delayed client payments.

What Operational Terms Are Commonly Used in Factoring?

Verification

Verification is the process of confirming that goods or services were delivered as stated. This prevents funding against fraudulent or disputed invoices.

Notice of Assignment (NOA)

A Notice of Assignment is a formal communication sent to customers informing them that their invoice has been assigned to a factor. It instructs them to send payment directly to the factor’s account.

Lockbox Account

A lockbox account is a bank account controlled by the factor where invoice payments are deposited. It ensures proper payment tracking and secure collection.

UCC Filing (UCC-1)

A UCC filing is a legal declaration giving the factor a security interest in the business’s receivables. It protects the factor’s rights over the collateral.

Concentration Limit

A concentration limit is the maximum exposure a factor allows toward a single customer. It manages risk by preventing reliance on one debtor.

Factoring Line (Funding Line)

A factoring line is the total amount of funding a client is eligible to access. It increases as more creditworthy customers and invoices get approved.

Buyout

A buyout happens when a new factor pays off the remaining balance owed to a previous factoring company. This allows businesses to switch providers without disrupting cash flow.

These operational terms define how factoring functions behind the scenes and ensure transparency between all parties.

When Do Businesses Use Factoring?

Businesses use factoring when long customer payment cycles create cash-flow gaps. The upfront advance helps cover expenses needed to operate smoothly.

It is also useful when a company cannot obtain traditional credit due to limited financial history. Factoring focuses on customer creditworthiness rather than the business’s own credit profile.

Industries like trucking, staffing, manufacturing, and wholesale distribution rely on factoring to support seasonal surges and ongoing operational demands. With the core and advanced terms defined, we can now look at how to choose the right factoring partner.

Check Routiqo Freight Factoring

Routiqo Freight Factoring Company helps owner-operators get paid without the usual delays that come with slow-paying brokers and shippers. Drivers get simple pricing, fast funding, and a team that actually understands life on the road.

Everything is built around making a trucker’s day easier, from quick invoice verification to having a real person pick up the phone when help is needed. The online portal keeps payments, invoices, and load details organized so drivers can focus on hauling instead of paperwork.

Routiqo also adds value with fuel advances, credit checks on shippers, and a free ELD device that never comes with monthly fees. With clear terms and support built for independent drivers, it feels less like a service and more like a reliable partner in your business.

Leave a Reply